James Handley coordinates the Carbon Tax Network. From its inception in 2007 until 2016, James served as policy analyst and Washington representative of the Carbon Tax Center. In that capacity, he attended Congressional hearings, studied and digested climate economics and climate policy literature; providing timely reports, summaries and blog posts for CTC's website while building a network of activists, academics and policymakers to support and advance transparent taxes on carbon pollution.

Prior to CTC, James represented environmental and citizen organizations, including Beyond Pesticides and the National Organic Consumers Association in public interest litigation. Prior to private law practice, he served 14 years at EPA, enforcing environmental law, where he also served as an officer in EPA's union, representing science and legal professionals, especially whistleblowers. Before law school, James specialized in environmental and energy-efficient design at Brown & Root, Inc. and Scott Paper Co. James holds degrees in Chemical Engineering (Economics minor), Law (JD), and Environmental Law (LLM, highest honors).

In a new research paper, posted last week, Dr. Hansen, who warned Congress about anthropogenic global warming in 1988, is taking on the mighty Intergovernmental Panel on Climate Change — the first and last word on climate science. Hansen points out how the IPCC process tends to understate climate risk, including instances where they’ve missed the boat, allowing a “wait and see” attitude to prevail.

That’s a new and dire observation. Though it was widely expected, given what we know about climate forcing feedbacks, including loss of ice albedo and increased methane bubbling up from arctic permafrost and released by unregulated fossil fuel drilling — especially fracking.

Until now, climate models have projected an essentially linear response to rising greenhouse gas levels. Hansen shows that in the past two decades global heating has started moving faster. Partly because we’re dumping more GHGs into the atmosphere, but perhaps even more alarmingly, because Earth’s climate system is measurably starting to feed back. That’s very bad news, and people whose livelihoods depend on pretending there’s a climate “solution” or that we can keep burning fossil fuels will not sit still for that.

He’s also saying that it’s still possible to stop that trend and even to reverse AGW. Even while admitting that Direct Air Capture and similar technologies cannot be scaled.

Hansen isn’t an expert on policy and economics, but he’s got the big picture. A carbon tax that can be globally harmonized is indeed still necessary. Hansen urges returning revenue through lump sum rebates, a policy choice that would forgo the vast benefits of reducing other burdensome taxes and replacing them with pollution taxes. Rep. John Larson, who may soon chair the House Ways & Means Committee, proposed exactly that in 2009.

I. Mainstream scientists are finally speaking and writing explicitly about catastrophic climate scenarios.

Until now — with a few exceptions — IPCC reports, other official publications, peer-reviewed science and economics have severely downplayed catastrophic climate risk. It started in 1979 with the first National Academy of Sciences report by the Charney Commission which mentioned the need for carbon taxes but recommended only “further study.”

The big models and studies assumed global warming would proceed on a more or less linear trajectory. Nope. That’s ignoring forcing feedback and tipping points. It’s a dangerous over-simplification; climate scientists knew that in 1979. (But don’t alarm the public. Or risk being called an “alarmist.” Besides, feedbacks and tipping points blow up our neat models.)

A new paper in Proceedings of National Academy of Sciences breaks the silence:

“Temperature rise has a wide range of lower probability but potentially extreme outcomes. Remaining blind to these scenarios is naïve risk-management at best and fatally foolish at worst.” —lead author Dr. Luke Kemp.

II. Democrats’ subsidy, subsidy and more subsidies climate bill, misleadingly titled the “Inflation Reduction Act” is not likely to help with inflation, though its methane fee will certainly help with climate.

The IRA’s major climate provisions are doing the easy thing, giving away money to renewable energy and rich drivers. It avoids the necessary thing– raising the cost to pollute.

“Democrats’ climate bill subsidizes non-fossil energy. But doesn’t recognize Climate Change as a global problem that requires cutting fossil fuel burning. A Carbon Tax is still necessary to actually solve the problem.” —Economist Tyler Cowen

A glaring problem with the IRA’s all-carrots, no-sticks approach: it doesn’t push consumers to conserve energy. Cheaper renewable energy will mean cheaper electricity and gasoline which encourages the opposite — it says “don’t bother to look for ways to cut waste or to improve efficiency.” Those “nega-watts” derived from conservation and efficiency are the cleanest energy in the world. No climate policy that ignores them can fairly be called “comprehensive” or even efficient.

And the bill’s “subsidy, subsidy and more subsidies” approach can’t be replicated across the globe. Even in the U.S., we can’t keep subsidizing non-fossil energy forever. As long as there’s more of the dirty stuff in the ground, and it’s cheap, someone will burn it. Subsidies for renewables increase total energy supply making dirty energy cheaper. That’s bound to be popular, but it’s not really climate policy, it’s more “all of the above” energy policy that brought us the fracking boom.

Unlike subsidies, a tax on climate pollution can go global, particularly if it becomes a revenue source for things voters want from government. Subsidies are only an option in rich countries; and even here they won’t do much for long. If we want to drive out fossil fuels not just spur renewables, we will need a carbon tax.

Subsidies often miss the mark. Think about ethanol. Congress enacted a subsidy and a mandate for adding ethanol to gasoline on the theory that it would displace (imported) petroleum. But for decades, numerous reports by the Congressional Budget Office have documented no climate and no energy benefit from the ethanol subsidy and mandate, mainly because growing corn for ethanol requires lots of fertilizer, almost entirely from natural gas. See e.g., Stop the Ethanol Madness The mainstay of the Renewable Fuel Standard is an unmistakable social and environmental failure. Why does it persist? (The Atlantic, November 2019.) Despite their cost and ineffectiveness, an entrenched lobby keeps ethanol subsidies and mandates going.

And how about the IRA’s subsidies for more attempts at thermodynamically bankrupt “Carbon Capture and Sequestration” demonstration projects? MIT professor Charles Harvey: “Every Dollar Spent on This Climate Technology Is a Waste.” CCS subsidies help justify continued production of coal, oil and natural gas at a time when the world should be ending its dependence on fossil fuels.

Expect more of those endless games with renewable and EV subsidies even if they don’t work as intended. Even before the IRA, it was clear that EV subsidies are going to the wrong drivers. As Kristen Eberhard at Niskanen Center reported, to maximize climate benefits, EV subsidies should go to heavy drivers, not to rich virtue signalers.

Subsidies make the politics of pollution taxes even harder by addicting renewable energy industries to subsidies, shielding them from the need to advocate and enact carbon taxes. A dozen years ago, we asked the American Wind Energy Association to support a carbon tax. Their reply: “Yes, it’s essential. Sorry, we’ve gotta keep our subsidies. We don’t want a fight with the fossil fuel lobby.”

And who benefits from subsidies? They’re terribly regressive.

“Energy subsidies are one of the few domains where there is a near full-throated consensus among progressives, governments, and economists over the need for reform. Nearly everywhere, energy subsidies are regressive, vastly favoring the car- and energy-consuming parts of the population that are often the least in need.” — From Regressive Subsidies to Progressive Redistribution: The Role of Redistribution and Recognition in Energy Subsidy Reform, NYU Center on Environmental Cooperation (November 2021.)

Though to be fair, the IRA does include a number of measures to help balance the distributional burden, so the goodies don’t all flow to the jet set and the Tesla crowd.

And while I rarely agree with Marc Thiessen, he hit the mark here:

“At a time when inflation is forcing many to choose between staples such as gas and food, the Biden administration is providing taxpayer subsidies to couples making $300,000 a year who can already afford a Tesla.”

And as Thiessen reports, despite its title as “Inflation Reduction Act,” various credible economic analyses conclude that the bill is not likely to reduce inflation.

By far, the best climate provision in the IRA is the methane pollution fee, crisply analyzed here, by the Congressional Research Service.

Methane is an extremely potent greenhouse gas, and in many places especially oil and gas drilling sites, it’s just vented to the atmosphere. New satellite imaging and atmospheric monitoring reveal that methane is a much bigger driver of global warming than was known even a few years ago. Equipment to capture methane is widely available and cost-effective, especially if drillers are prodded by a hefty and rising methane pollution tax. Enactment and success of a methane pollution tax could set a precedent for a carbon tax.

III. And yes, we still need that carbon tax.

Another nice try: Senator Sheldon Whitehouse (D-RI) proposed a Carbon Border Adjustment Mechanism, called the Clean Competition Act, a tax on carbon-intensive imports along with an equivalent tax on similar domestic goods. I recommend the short summary by Niskanen Center’s Shuting Pomerleau. And here’s trade expert Jennifer Hillman explaining and extoling CCA: “Congress can address competitiveness and climate change — without breaking trade rules.”

So here we are. Facing the prospect of near-term human extinction. Today, Senate Democrats passed the “Inflation Reduction Act” without a single Republican vote. A bill that offers voters a measure of hope that Senate Democrats can address climate breakdown, strictly along partisan lines. And without the key policy that the NAS Charney Commission identified 43 years ago as essential to avoiding and curbing runaway global warming — a rising carbon tax to make climate polluters pay so renewable energy and efficiency can compete fairly and phase out fossil fuels.

So, here’s one cheer for the Inflation Reduction Act!

And here’s to electing a more responsive Congress in November. For years, polls have shown strong public support (roughly 2/3) for taxes on climate pollution. And yet it didn’t make the cut in the Democrats’ bill. (Was it Manchin, or some other Democrat who torpedoed a carbon tax? It certainly was discussed.)

Similarly, voters have long shown strong support (again, about 2/3) for the reproductive freedoms that until last month were guaranteed by the Supreme Court in Roe v. Wade. I hope the voters in Kansas, who this week resoundingly rejected and overcame the disastrous and politically reckless Supreme Court overruling of Roe v. Wade, are leading the way. Maybe, just maybe, a wave election in November could open the way for truly effective and globally harmonizable climate policy — a hefty and rising carbon tax.

Guido Girgenti, Media director of Justice Democrats. Founding board member of Sunrise Movement.

Book Review: Winning the Green New Deal (Part 3 of 3)

Neo-liberalism, also known as “de-regulated capitalism,” has been the predominant ideology of both major U.S. political parties since the Reagan revolution four decades ago, according to the Sunrise Movement’s political advisers Guido Girgenti and Waleed Shahid. Their chapter, “The Next Era of American Politics,” cites Charles Peters’ seminal “Neo-liberal Manifesto” published in 1983 by Washington Monthly, then a nascent neo-liberal standard-bearer. Peters’ lengthy, erudite essay questioned many established Democratic Party doctrines such as support for labor unions, activist government and regulation of commerce that had bound together the New Deal coalition. Peters also urged Democrats to loosen their adherence to the civil rights principles and social programs of the Great Society era. Peters called on Democrats to co-opt much of what he viewed as Reagan’s common-sensical and politically-savvy ideology. Speaking for what became the “New Democrats,” Peters proclaimed, “We will no longer automatically favor unions and big government or oppose the military and big business.” Reagan (and alas, Clinton’s) dog-whistles added an even harsher note to neo-liberalism: strategic racism in order to sow distrust in government. Right-wing “think tanks” like the Heritage Foundation emerged to fan the flames of racism and anti-abortion fervor that serve as wedges to divide the middle class in order to advance “free-market” ideology and weaken government, benefiting entrenched fossil fuel interests and the wealthiest.

Girgenti and Shahid argue that President Clinton turned Reagan and Bush’s ideology into conventional political wisdom, for example by implementing fiscal austerity and deregulating financial markets. George W. Bush continued those trends, adding endless war to the neo-liberal portfolio by invading Iraq.[1] Confronting the 2008 financial crisis, Barack Obama ran on a more activist government, but his administration quickly hewed to the neo-liberal norm. Girgenti and Shahid make a strong case that even under Trump, American politics is “still playing out the Reagan era.” But they point out that our current convergence of economic, political, climate and now COVID-19 crises may — like the bleak conditions of the Great Depression that preceded FDR’s New Deal — offer a rare opportunity for organizing a political re-alignment. FDR’s election and key elements of the New Deal emerged only after U.S. industrial production had dropped from $949 million to $74 million in just three years. The pain was palpable to everyone. In practically every major city, unemployed, hungry people set up encampments known as “Hoovervilles,” named for the GOP president who steadfastly refused to intervene, claiming that government intervention would only distort markets and prolong the crisis. Girgenti and Shahid argue that in the same way the crushing conditions of the Great Depression loosened the grip of Herbert Hoover’s laissez-faire ideology, the current economic, public health and climate crises offer a chance to break the shackles of neo-liberalism that have held back effective government interventions for the past four decades.

In “People Power and Political Power,” Varshini Prakash recounts how in just two years, the Sunrise Movement has begun to build an intersectional alignment of civil rights, women’s rights, climate justice and economic justice activists who have been alienated, even oppressed by neo-liberalism. Prakash points out that while Speaker Pelosi intones that she “believes the science” of climate change, she is not advancing policies that seriously confront the climate crisis, perhaps because Pelosi’s career has been subsumed within four decades of neo-liberal dominance.[2] Prakash questions whether Pelosi, who maligned Sunrise’s proposal as the “Green Dream or whatever it’s called,” can see beyond the confines of the neo-liberal fog she has always inhabited.

In November 2018, by occupying Speaker Pelosi’s office, with the enthusiastic participation of newly-elected Rep. Alexandria Ocasio-Cortez, Sunrise kicked off a movement that aims to re-align the Democratic Party into the party of the Green New Deal. In March 2019, Sunrise and other climate activists occupied Senator Feinstein’s office urging her to endorse the GND. In a confrontation that went viral, Feinstein rudely brushed off the young activists, telling them that she knew better what could pass the Senate. Last January, Sunrise endorsed GND advocate Bernie Sanders for president, adding their organizing firepower to his campaign, especially in Iowa, New Hampshire and Nevada and launching the GND into mainstream press coverage and the Democratic debates.

Jamaal Bowman, who won the primary for NY-16

One of Sunrise’s key tools is the same one used by the right-wing Tea Party: supporting primary challengers of incumbents. In just the few months since “Winning the Green New Deal” was written, Sunrise has put its activist boots on the ground with dramatic results in several key primaries. After Jamaal Bowman, a Bronx middle school principal endorsed the GND, Sunrise campaigned aggressively with him, defeating Eliot Engel, a 30-year incumbent who chaired the House Foreign Affairs Committee.

Sunrise co-founder Varshini Prakash with Senator Ed Markey

And just a month ago, Sunrise propelled GND supporter Senator Ed Markey to victory over challenger Joe Kennedy, whose family name recognition in Massachusetts had been considered an almost insurmountable advantage. Sunrise also supported Alex Morse, mayor of Holyoke, Massachusetts, who ran on a GND platform prodding Rep. Richard Neal, chairman of the powerful House Ways and Means Committee to address climate policy in his campaign. After state Rep. Charles Booker, the youngest black state lawmaker in Kentucky, endorsed the Green New Deal and Medicare for All, Sunrise pulled him within striking distance of Democratic Party favorite Amy McGrath who prevailed in the June primary and is now challenging Majority Leader Mitch McConnell for Senate his seat.

I strongly recommend “Winning the Green New Deal” for its diverse, inside look at a growing and hopeful youth-led movement that for the first time boldly advocates policies on a scale and in a time-frame commensurate with the accelerating climate crisis.

Thanks to the Sunrise Movement, the Green New Deal vision which Speaker Pelosi ridiculed and Senator Feinstein brusquely dismissed, can no longer be ignored. It remains to be seen whether Joe Biden and the Democratic leadership on Capitol Hill can be pushed to move beyond the ideology and political habits that have hamstrung government action on climate and social justice for four decades. That portends a long but necessary struggle.

NOTES:

[1] Senator Joe Biden, chair of the Foreign Relations Committee in 2002, established the pretext for Bush’s invasion by calling witnesses who falsely claimed that Iraq possessed weapons of mass destruction and that Iraq was harboring Al Qaeda terrorists. Biden refused to call U.N. weapons inspectors and State Department experts who knew better. Biden’s leadership of the resolution authorizing Bush to invade Iraq is crisply documented by video of the Senate hearings in “Worth the Price,” a 19-minute mini-documentary by Mark Weisbrot.

[2] Similar to Sunrise’s effort to launch primary challenges to incumbents, peace activist Shahid Buttar launched a primary challenge to Speaker Pelosi. Confronting Pelosi’s continued authorization of military budgets funding endless war, Buttar won the right to run against Pelosi in the November general election, a ballot slot which California election law awards to the candidate with second-highest vote total in the primary.

Book Review: “Winning the Green New Deal” (Part 2 of 3)

Writer and climate activist Bill McKibben opens the “Visions and Policies” section of “Winning…” with his chapter, “How We Got to the Green New Deal,” tracing the emergence and current standoff of the U.S. climate movement. McKibben begins with the summer of 1988 when NASA climate scientist James Hansen famously warned the Senate about the catastrophic consequences of global warming. Within a year, McKibben sounded his own alarm, his best-selling book, “The End of Nature.” Looking back, McKibben laments that “fairly modest” steps such as a pollution tax on CO2 and methane, if taken thirty years ago, would now be “scrubbing fossil fuel out of our economy,” putting the world “well the way” to tackling global warming.

Writer and Climate Activist Bill McKibben.

McKibben admits that he and other climate activists were naïve to take at face value President Bush’s 1989 vow that the “greenhouse effect would be met by the White House effect” and to place so much stock in the 1997 Kyoto Protocol which the U.S. systematically evaded and undermined. As revealed since then, even when Dr. Hansen testified in 1988, Exxon’s own scientists already had accurately estimated how fast the global climate was warming; the company even factored sea-level rise into design of its offshore drilling rigs. Meanwhile, the public face of the fossil fuel industry followed the “tobacco war” strategy: stirring up spurious uncertainty and denying the existence and seriousness of global warming. McKibben’s history culminates with the U.N.’s 2009 Copenhagen climate summit which deadlocked, accomplishing “essentially nothing.” And yet, even after the Senate subsequently abandoned the House-passed cap-and-trade legislation, the climate movement garnered victories in fighting the Keystone XL pipeline, and Alexandria Ocasio-Cortez credits her radicalization on climate to participation in the Dakota Access pipeline fight.

McKibben traces both climate science denial and rising income inequality to the Reagan revolution. These “two great disasters of our time” he writes, were abetted by the fossil fuel industry, especially the billionaire Koch brothers, whose largesse funds countless front groups to “block renewable energy, defund mass transit, trash environmentalists and enact tax cuts for the rich, while depressing social spending.” After pointing out how escalating economic insecurity has fostered public resistance to any kind of economic restructuring, including effective climate policy, McKibben concludes that only by simultaneously tackling both climate injustice and economic injustice can we break the gridlock that the Koch brothers orchestrated.

Rhiana Gunn-Wright, Green New Deal Architect, Director of Roosevelt Institute.

Continuing the book’s second section, Rhiana Gunn-Wright, Green New Deal architect, former Rhodes Scholar and policy director of the Roosevelt Institute, outlines the “Policies and Principles of a Green New Deal.” She expects a rapid shift away from fossil fuels, which power virtually everything (because the U.S. derives only 11% of its energy from renewables), will be hugely disruptive, especially to marginalized people who are already struggling. Therefore, she argues, “the Green New Deal can only succeed if it is just and equitable,” increasing everyone’s economic security in a full-scale economic mobilization that protects front-line communities and rapidly boosts employment.

Joseph Stiglitz, Nobel-prize winning economist.

Making “The Economic Case for a Green New Deal,” Nobel-prize winning economist Joseph Stiglitz critiques conventional economic analysis which he concludes has downplayed the “fat tail” (catastrophic) risk of unmitigated climate change by excessively discounting future climate damage and other accounting tricks. Standard economic models “fail to recognize the complex feedback mechanisms, non-linear effects, and tipping points in our climate system,” he says. Sweeping aside the notion that we can’t “afford” a Green New Deal, Stiglitz recalls that our leaders didn’t dither over questions about whether we could afford to fight the Second World War; FDR and Churchill knew the cost of losing would be staggering.

Stiglitz points out that high unemployment and a surfeit of un-invested savings offer ideal conditions for the massive public investment needed to transition to a green economy, concluding with the hope that “deficit fetishism seems finally to be over.” Sticking to conventional Keynesian analysis, Stiglitz sidesteps the controversy over “Modern Monetary Theory.” He is confident that it would be “easy” to raise revenue to finance public investment in fighting climate change while increasing economic efficiency by “taxing dirty industries, imposing a broad range of taxes on pollution and on destabilizing short-term financial transactions and by closing tax loopholes that allow highly profitable corporations to get away with paying almost no taxes…”

Collette Pincon-Battle, Director of Gulf Coast Center for Law & Policy.

In “A Green New Deal for the Gulf South,” Collette Pincon-Battle, Director of the Gulf Coast Center for Law & Policy, envisions what a Green New Deal would mean for her region, which prospers from fossil fuel extraction (the Gulf South includes 45% of US petroleum refining capacity) while also suffering its environmental and health consequences and now faces massive climate damage from increasingly severe hurricanes, flooding and displacement due to sea-level rise. Battle suggests that by revitalizing the region’s economy, the Green New Deal can be understood as a form of reparations for black southerners. She acknowledges the “centrality of the military in Gulf South communities,” urging a transition “away from the military and toward job creation in regenerative local economies.”

Julian Brave Noisecat, Vice President of Policy and Strategy at Data For Progress.

In “Green New Bingo Hall,” Julian Brave Noisecat, Vice President of Policy and Strategy at Data For Progress, reminds us that we’re gambling on a global scale: Since 1988, when Dr. Hansen testified to the Senate, we have spewed more carbon into the atmosphere than during all of prior human history. And we’re not slowing down. Thanks to fracking, the U.S. is now the world’s largest oil producer, a “petro-state” or as NoiseCat more aptly puts it, a “necro-state –a uniquely destructive force in global history.” Noisecat recounts indigenous-led struggles against the Keystone XL and Dakota Access pipelines and mentions that Alexandria Ocasio-Cortez attributes her climate radicalization to that experience. He urges a Green New Deal built with instead of for indigenous peoples, “honoring the treaties, the tribes, the rivers from which we drink, the air we breathe, and land where we plant and gather our food and to which we return when our time is up.”

Mary Kay Henry, President, Service Employees International Union.

The final chapter of the “Visions and Policies” section of “Winning the Green New Deal” is “A Workers’ Green New Deal” by Service Employees International Union president Mary Kay Henry. With the Wagner Act of 1935, the New Deal Congress established the right to collective bargaining. But since the Reagan administration, federal policies have weakened labor unions and workers’ right to collective bargaining. In 1953, 35% of U.S. workers were represented by labor unions, now that figure has dropped to just 11%. And now almost half of the U.S. workforce earns a paycheck doing service and care work. Ms. Henry points out that the same forces that have crippled labor rights also fund climate science denial and fan the flames of racism. The results: More people working for lower wages, many in places increasingly vulnerable to climate disasters that disproportionately affect low-wage workers and communities of color. She is proud that SEIU stood with the Sioux and climate activists at Standing Rock and also cites SEIU’s successful 2013 strike by New York restaurant workers to enact a $15 wage. She praises the German model of sector-wide labor unions as a means to negotiate job standards with employers in order to transition both workers and employers away from dirty energy sources.

Book Review: “Winning the Green New Deal” (Part 1 of 3)

If accelerating carbon pollution is turning Earth’s climate into an unlivable, churning hell, shouldn’t promptly stopping that pollution take priority over other problems such as healthcare, education, inequality and systemic racism? In “Winning the Green New Deal,” a collection of essays compiled by Varshini Prakash and Guido Girgenti, co-founders of the youth-led Sunrise Movement, diverse activists, academics and journalists reply with a resounding: HELL NO!

Their message: These struggles are inextricably linked; we must unite to re-take our country and save our planet.

Varshini Prakash, co-founder, executive director, Sunrise Movement

Their arguments are not merely political (e.g., the need to build broad coalitions) and moral (climate policy should not make other problems worse, especially for the disadvantaged). Their case also rests on economic footings (with record-level unemployment and mountains of cash parked on sidelines, we have plenty of idle labor and capital available to rebuild and “green” our infrastructure), and psychological grounds (human civilization depends on cooperation at least as much as competition).

Ultimately, the book challenges us to re-imagine the role of our government as much more than a tool to foster economic growth.

The book is organized into three sections, describing the “why,” “what” and “how” of winning the Green New Deal. In Chapter One, “The Crisis Here and Now,” reporter and author David Wallace-Wells sounds a “deafening, piercing alarm” about the “cascade of cruelties” already buffeting humanity. One example of the ferociously-accelerating pace of global warming: In the past five years, Houston has been hammered by five disastrous hurricanes of a magnitude that was previously expected only once every 500 years.

In Chapter Two, “We Didn’t Start the Fire,” Kate Aronoff lays groundwork for a major thrust of the book: We need a full-scale, government-led intervention even to mitigate the climate crisis. Urging a renewal of the cooperative spirit of the New Deal, she quotes FDR economist Rexford Tugwell (1934): “Laissez-faire exalted the competitive and maimed cooperative impulses. It deluded [us] with a viciously false paradox: the notion that the sum of many petty struggles was aggregate cooperation. The cooperative impulse [must now] assert itself openly.”

Naomi Klein, author, social activist, filmmaker.

In Chapter Three, “Market Fundamentalism at the Worst Time,” Naomi Klein sifts through the rubble resulting from four decades of neo-liberal policy, showing how the ideology of “free” markets and government austerity has systematically demolished the New Deal structures that fostered the kind of cooperation now needed to tackle climate breakdown.

Prof. Ian Haney Lopez, author of “Dog Whistle Politics” (2014)

Chapter Four, “Averting Climate Collapse Requires Confronting Racism” forms a linchpin of the book. In just 14 pages, law professor Ian Haney Lopez traces the GOP’s strategic use of racism over the past 4 decades. Ronald Reagan peppered his speeches with dog whistles like, “Cadillac driving welfare queens” or “strapping young bucks buying T-bone steaks with food stamps” to sow distrust in government, shattering the original New Deal coalition. Lopez reveals the dirty trick of dog-whistle politics: coded racial messages that benefit plutocrats by prompting enough white people to vote their racial fears over their own interests, values and beliefs. In a stunningly candid 1981 interview, Lee Atwater, Reagan’s political adviser and later chair of the Republican National Committee, confessed the strategy. As overt racism, such as chants of “nigger, nigger, nigger” became unacceptable, the wording shifted to “states’ rights” then to “forced busing,” and now to “cutting taxes” built on the coded (and false) subtext that “blacks get hurt worse than whites” when government is hamstrung. Now, strategic racism, funded by fossil fuel interests, including climate-science denying coal magnates like Koch Industries, is thwarting efforts to end the fossil fuel era.

Prof. Lopez takes pains to point out that it’s not necessary for dog whistlers to personally harbor racial animus in order to make strategic use of coded racial messages. Debate about what’s “in someone’s heart” (i.e., whether a particular politician hates people of color) is beside the point. If we know what to listen for, it’s clear that Donald Trump and nearly all GOP politicians (and, alas, too many Democrats) use racial code to motivate their base, regardless of their personal attitudes toward any particular racial or ethnic group.

Lopez outlines three elements of these coded racial messages: “1) Fear and resent people of color, because they’re basically violent and lazy, 2) Distrust government, because it coddles and refuses to control these undeserving minorities, and 3) Trust the marketplace because markets reward hard work. Support the very wealthy and large corporations because they are the job creators.” So when we hear politicians describe the George Floyd / Black Lives Matter protesters as “violent looters,” the same politicians who call for more tax cuts, austerity and abandonment of the social safety net while extolling “free markets” and global trade deals that outsource jobs, we know what’s going on. They’re dividing voters along racial lines in order to grab more power and profit for the top one percent.

Lopez concludes that creating the progressive wave needed to win a Green New Deal requires mobilizing a broad movement that “rejects division in favor of cross-racial solidarity.” That movement must, he says, tackle racism. He offers a countervailing narrative: “1) Distrust greedy elites who sow division. 2) Join together across racial lines. 3) Demand that government work for all racial groups, whites included.”

Is there a “middle way” to effective climate policy? A policy that makes sense regardless of whether you’re panicking over mass extinction or not quite sure the climate threat is serious? A policy whose cost-effectiveness[1] predominates over other policies so strongly that it appeals to both small government conservatives as well as environmental activists?

In his new book, “Paying for Pollution,” economics professor Gilbert E. Metcalf lucidly demonstrates why a well-designed carbon tax is that middle path. And, he shows why there are no good alternatives if we are serious about curbing our growing exposure to climate risk.

Prof. Gilbert E. Metcalf, Tufts University.

Metcalf certainly knows the features and pitfalls of the carbon pricing terrain. For two decades, he has focused on the role of tax policy to correct market failures. (A decade ago, after hearing his testimony encouraging the House Ways & Means Committee to propose a simple carbon tax or to simplify the behemoth cap-trade-offset bill emerging from the Energy & Commerce Committee, I had to resist the urge to stand up and applaud.) And he’s served in government, as Deputy Assistant Secretary for Environment and Energy at the U.S. Treasury from 2011-12.

Metcalf opens his book with a bird’s eye view of climate science, which through an economic lens, is telling us that we face serious and growing climate risk. That risk comes in the form of “known unknowns” such as more frequent and more damaging events like storms, floods, droughts and wildfires as well as “unknown unknowns” such as rapid methane release from Arctic permafrost and ocean clathrates. By analogy to Blaise Pascal’s famous theological wager about the existence of God, Metcalf suggests that even climate science skeptics would be wise to hedge their bets by supporting least-cost climate policy, for the same reasons they would buy fire insurance for their houses.

Metcalf introduces us to Ronald Coase, awarded a Nobel in 1991 for the insight that pollution rights can be allocated efficiently only if the parties hold explicit property rights, allowing them to negotiate. Next, we meet Arthur Pigou, who first observed that taxing pollution instead of beneficial activities can improve aggregate welfare by discouraging and reducing the unpriced costs of pollution. Pigou’s further insight was that the benefits of pollution taxes can offset much (sometimes all) of the economic drag normally associated with taxation.

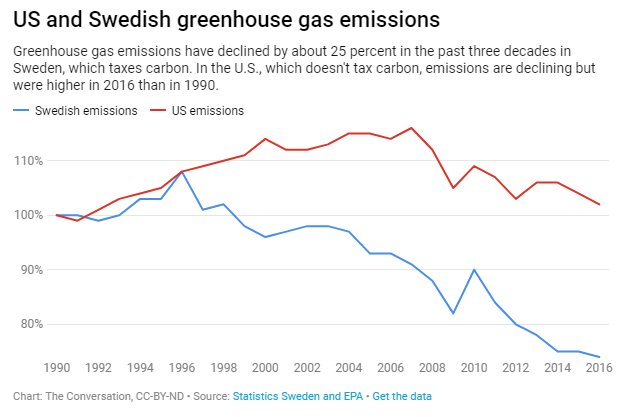

Having neatly laid that groundwork, Metcalf turns to a real-world example: Sweden, which imposed a hefty $130/t CO2 tax in the early 90’s, using the revenue to reduce other taxes and equalize tax burdens. Sweden’s carbon tax has gradually but dramatically reduced its CO2 emissions, even as its economic growth has surged along a similar trajectory to that of the U.S.

Similarly, British Columbia imposed a revenue-neutral carbon tax in 2008 that has apparently reduced the province’s emissions while its economic growth exceeded the rest of Canada.

Paying For Pollution, Oxford Press (2019)

My favorite of Prof. Metcalf’s chapter titles is “Isn’t There a Better Way? (No, There Isn’t)” Here, Metcalf sets forth four criteria for climate policy. First, it should actually reduce emissions. Second, it should be cost-effective, delivering maximum efficacy per cost. Third, it should encourage innovation. And finally, it should be simple and transparent, to minimize administrative burdens and costs while limiting gaming and political meddling.

Metcalf walks us through real-word examples of alternatives to carbon pricing: regulations and subsidies. As examples of regulations, Metcalf examines performance standards and technology mandates EPA issued under the Clean Air Act. These encourage industry to comply by adopting the technology that EPA used to establish the standard; thus they don’t encourage much innovation. One example is the 1977 Clean Air Act mandate for power plants to install equipment to reduce sulfur emissions by 70 – 90%, regardless of the initial emissions rate. Congress chose this mandate to protect high sulfur eastern coal. Under the rule, dirty power plants that were burning high sulfur coal as well as cleaner ones that already had reduced emissions rates by burning low sulfur coal were forced to install scrubbers.[2] Metcalf points out estimates that it would cost roughly half as much to price sulfur dioxide emissions and let power plant operators choose whether to reduce emissions by installing scrubbers or buying western low-sulfur coal.

Automobile fuel efficiency (“Corporate Average Fuel Efficiency” or “CAFÉ”) standards might seem reasonably cost-effective, but because Congress included an exemption for light trucks, CAFÉ standards encouraged a perverse boom in gas-guzzling SUV sales. And the mandate for more efficient vehicles without a price on carbon has created a rebound effect. People drive their more efficient cars more miles, eroding net emissions reductions. Metcalf cites a study by Resources for the Future concluding that the average cost of reducing a ton of CO2 emissions via CAFÉ standards is about $85/ton, while a carbon tax would do the job for only $12/ton.[3]

Other alternatives to carbon pricing include subsidies and mandates. State-imposed Renewable Portfolio Standards (RPS’s) require utilities to generate a specified fraction of electricity from renewable sources. Metcalf points out that these rules do not encourage consumers to conserve electricity. A new study found that to reduce carbon emissions from electricity generation by 10%, an RPS program costs six times what carbon tax would.[4]

The federal government offers subsidies in the form of Production Tax Credits (PTC’s) to generators of wind and solar power. But by putting more power on the grid, the PTC reduces electricity prices, thereby increasing demand. Subsidies for hybrid cars mostly benefit the wealthy; with or without the subsidy they are the market for expensive hybrids. And policy interactions can create perverse incentives. Because CAFÉ imposes average fuel efficiency on each manufacturer’s fleet, selling an efficient hybrid in one place allows that manufacturer to sell an additional gas guzzler somewhere else.

On the “innovation” criterion, Metcalf points out the deep body of research concluding that zero-carbon energy R&D in both the public and private sector are woefully underfunded in terms of cost vs social benefits. By predictably increasing the cost of fossil fuels, whose prices now undercut cleaner alternatives, a carbon tax would provide incentives for private investment in clean energy R&D. Metcalf suggests the revenue from eliminating fossil fuel subsidies as a source of funds for public investment in clean energy R&D.

Having demonstrated the advantages of carbon pricing over regulations, subsidies and mandates, Metcalf proceeds to compare quantity-based carbon pricing mechanisms (caps) with price-based mechanisms (taxes). In theory, Metcalf concedes, a cap-and-trade system can price carbon just as efficiently as a carbon tax. But in practice, the results of cap-and-trade have not been impressive. Both the California system and the European Union’s “Emissions Trading Scheme” have been plagued by price volatility and carbon prices too low to have much effect on demand or innovation. To stabilize prices, “collars” have been added to both systems. When triggered, an upper price limit effectively releases the emissions cap by issuing more allowances. And a price floor obligates the government to buy back allowances in order to prop up market prices. Thus, a cap-and-trade system with a price collar operates like a tax with a lot of needless complexity that increases opportunities for fraud and abuse. Metcalf also points out that only a carbon tax continues to prod further reductions even when standards, regulations and mandates have been met.

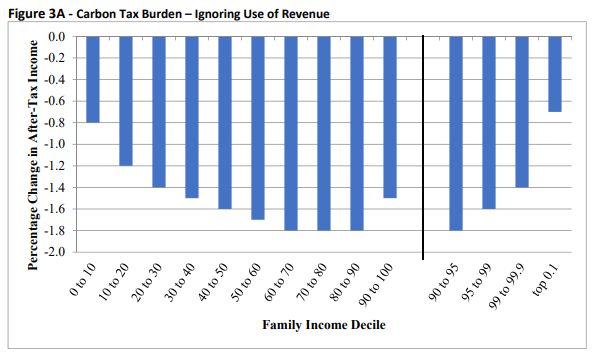

Metcalf next tackles the thorny question of revenue. He begins by citing an authoritative study issued by the Treasury Department in the waning days of the Obama Administration, concluding that the incidence of a carbon tax is distributionally-progressive. High income households would pay proportionally more carbon taxes than low and moderate-income households all the way up to the 95th percentile of income. Within the top 5%, the distribution becomes regressive, presumably because that top 5% are constrained by some other variable, like time. (Maybe one can only take so many globe-trotting flights in a day.)

Source: U.S. Department of the Treasury (2017)

When revenue from a carbon tax is returned via equal lump sum rebates (a.k.a., “dividends”) the net distributional effect becomes even more progressive. Another option is to use the revenue to reduce the top marginal corporate income tax rate. Not surprisingly, this option is regressive, but would have offered large efficiency benefits. Alas, Congress cut the corporate income tax rate in 2017 (without paying for the expenditure, thus substantially increasing the deficit) seriously blunting the efficiency argument for using carbon tax revenue to further cut corporate income taxes. Perhaps surprisingly, Metcalf’s book does not mention his proposal from a decade ago to use carbon tax revenue to rebate payroll taxes, an option that he showed would be distributionally-progressive and which was incorporated into a bill introduced by Rep. John Larson (D-CT).

Metcalf overviews “best practices” for carbon tax design. His touchstones are administrative simplicity, low compliance costs, broad coverage (avoiding exemptions) and a substantial enough price signal to actually reduce (and continue to reduce) greenhouse gas pollution. For simplicity, a carbon tax should be imposed at the narrowest point in the respective supply chains of coal, oil and natural gas – where there are fewest taxpaying entities. Metcalf suggests including some non-CO2 greenhouse gases, including fluorocarbon refrigerants. But he concludes that to discourage fugitive methane emissions from oil and gas wells and gas distribution systems, technology-based regulations make more sense than a tax. Metcalf invokes the standard free trade based arguments for border tax adjustments which would exempt exports from carbon taxes to avoid putting them at a competitive disadvantage,[5] while imposing carbon taxes on energy-intensive imports in order to avoid favoring imports.

The carbon tax rate and its rate of increase are rivaled only by broad coverage as a crucial design elements to assure effectiveness at reducing emissions. Metcalf suggests skipping over the controversy and uncertainty[6] surrounding how to estimate the “social cost of carbon,” instead just choosing a future emissions target and periodically adjusting the tax rate along the way to stay on track.

In a chapter titled “Objections to a Carbon Tax,” Metcalf debunks the myth that carbon taxes will hurt the economy or “kill” jobs. Citing standard macro-economic models, Metcalf assures us that economic growth will overwhelm whatever small economic drag might be created by carbon taxes. And that analysis does not include the much larger benefits of reducing future climate damage. Metcalf agrees that transition assistance is needed for coal miners and other fossil fuel workers displaced by the transition to low or zero-carbon energy, but he is quick to attribute the lion’s share of coal job losses to the shale-gas boom that has driven natural gas down to prices that encourage utilities to replace coal-fired generation with gas. He points out that the transition to a low carbon economy will create far more jobs in renewable energy than are lost in fossil fuel related sectors.

Metcalf also deftly dispatches the argument that a carbon tax imposed by the U.S. wouldn’t matter. He points out that border tax adjustments offer a prod to other nations to enact their own carbon taxes, and he assures readers that leadership by the world’s largest economy really does matter, perhaps especially on climate policy.

In his final chapter, Metcalf offers a passing glance at the elephant in the room – political resistance to carbon taxes.[7] He recalls the two principles of President Reagan’s 1984 speech which spurred Congress to enact comprehensive tax reform two years later. First, the reform had to be revenue neutral, and second, it had to lower tax rates by broadening the tax base and cutting out loopholes. Metcalf suggests that in order to sidestep the politically-charged debate over the “size of government,” carbon taxes should also be revenue-neutral.[8]

Metcalf says his biggest worry about climate policy is not that we will not enact it, but rather that we will choose inefficient policies. Noticeably absent from Metcalf’s carefully-balanced map of the “middle way” to a carbon tax is an appeal to the environmental left. Judging by reports about the “Green New Deal,” progressives seem to be jumping on the bandwagon for a range of inefficient and possibly ineffective regulations, subsidies and mandates. Some advocates have even gone so far as to explicitly exclude carbon taxes.[9] Maybe Metcalf is right to be worried.

FOOTNOTES:

[1] Readers (like me) who are more concerned about environmentally effective climate policy than about efficient (low-cost) policy can safely substitute the word “effective” in the many instances where Metcalf points out the efficiency (or cost-effectiveness) of carbon taxes. My assumption is that in a world where climate policy is constrained by political ambition, the most efficient policy is also the most effective. Of course, we climate hawks still have our work cut out to ensure and maintain an aggressively-rising carbon price, but the efficiency advantage of a carbon tax will pay off at any given level of political ambition.

[2] Metcalf notes that Congress eliminated this perverse provision in the 1990 Clean Air Act Amendments.

[5] In “Can We Price Carbon?”(2018) political scientist Barry Rabe points out the popularity of ad-valorem severance taxes imposed at the point of fossil fuel production in states including Alaska, North Dakota, Wyoming, Oklahoma, Texas and California. Rabe points out that these severance taxes could easily be converted to carbon taxes by changing their basis from the dollar value of the fuel to its carbon content. Either way, their burden would continue to fall largely on out-of-state fuel consumers while funding popular programs in the states imposing them. For instance, Texas endows its Permanent University Fund with revenue from oil & gas severance taxes. This suggests that a carbon tax without a border tax adjustment to return tax revenue to producers of fuel for export might be more politically popular than a standard WTO consumption-based tax.

[6] Metcalf cites MIT economist Robert Pindyck, who has called the models used to estimate climate damage and the social cost of carbon “close to useless,” but who nevertheless argues forcefully for a carbon tax despite uncertainty about the “optimal” rate.

[7] For a terrific political science overview of carbon pricing successes and failures, see “Can We Price Carbon?” (2018) by Barry Rabe, which I’ve reviewed here.

[8] In a footnote, Metcalf concedes that by consistently approving increases in military spending and in 2017 by enacting tax corporate tax reductions that substantially increased the deficit (and overwhelmingly benefit the wealthiest households), Republicans have given fodder to liberals who question the good faith of Republican insistence on “small government” and their avowed aversion to deficits. Nevertheless, Metcalf insists that “this debate should have nothing to do with climate policy.”

[9] See Grist, “Is the Green New Deal the Only Way Forward?” (December 10, 2018), quoting Evan Weber, “We’ve seen that carbon taxes are not winning elections, and they’re not winning at the ballot.”

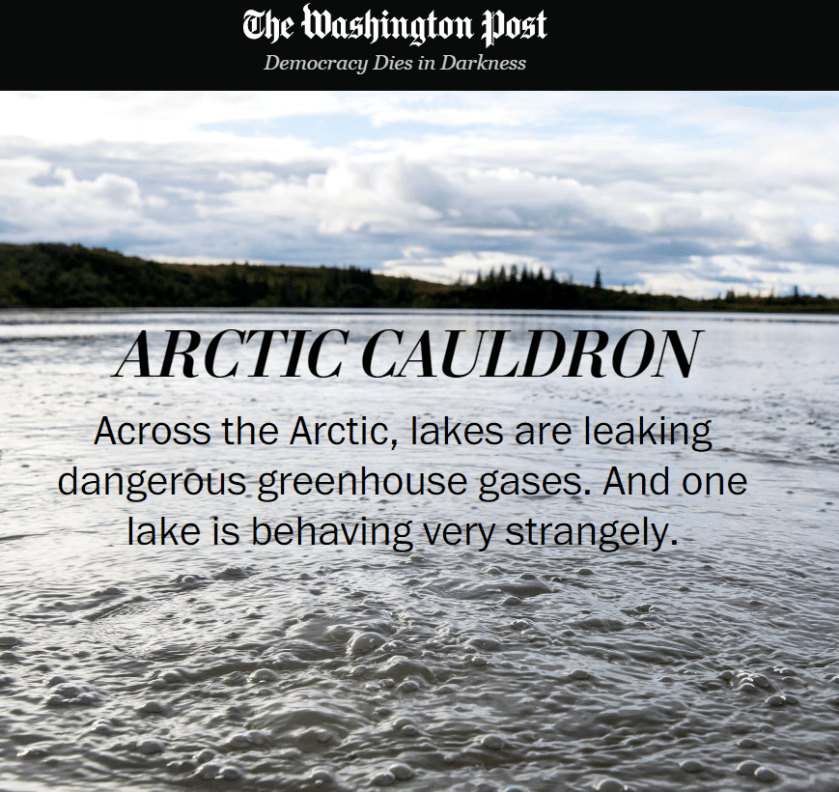

If donning a wetsuit and diving into an Arctic lake to get a look at underwater craters boiling up methane gas sounds like an exciting adventure, let me introduce you to Katey Walter Anthony,[1] who did just that in an Alaska lake last summer. Last week, Dr. Anthony took a break from the meeting of the American Geophysical Union here in Washington, to offer a short briefing where she explained what she found.[2]

Dr. Katey Walter Anthony (National Geographic)

A bit of background: Methane (“natural gas”) like carbon dioxide, is a greenhouse gas. Greenhouse gases block infra-red radiation, reducing the amount of heat escaping from earth’s surface into space: Global warming. Methane is a more potent greenhouse gas than carbon dioxide, but it breaks down much faster.

Dr. Anthony has been studying the dynamics of Arctic lakes for a couple of decades. Thermokarst lakes form when arctic soil begins to thaw, leaving voids where ice crystals have melted, causing the soil to subside. Last year, native Alaskan groups contacted Dr. Anthony seeking her help finding methane seeps which they hope to use as fuel in their remote villages.[3] As lake bottoms thaw due to a warming climate, partially-decayed plants and animals, until now locked in permafrost, are starting to thaw and resume their decay, releasing carbon dioxide and methane. Increasing release of carbon dioxide and methane from thawing permafrost is one of about half a dozen amplifying climate feedback mechanisms that scientists have documented and begun to quantify.[4]

But what Dr. Anthony found at a lake that she named Esieh, just above the Arctic Circle, is even more troubling. She spotted the telltale signs of methane release — photos show that the lake doesn’t freeze over. And when she and her team arrived to set up camp, they were greeted by a steady eruption of grapefruit-sized bubbles rising to the lake surface. Carbon dating reveals that the gas is fossil methane, not the product of decaying material in permafrost, but gas from deeper geologic formations. Dr. Anthony surmises that as permafrost melts, it unseals fissures and crevices that connect to geologic gas deposits.

It’s not clear yet whether Esieh Lake is an anomaly, or part of a larger pattern of thermokarst lakes with underground connections to geologic methane, which would have ominous implications for earth’s climate. What we do know, as Dr. Walter put it, is that “these lakes speed up permafrost thaw. It’s acceleration.” And that the amplifying effects of releasing fossil methane at an accelerating rate are not included in current climate models.[5]

That’s not a rhetorical question. Jurisdictions around the globe have struggled for more than two decades to price carbon emissions. The results are mixed and frankly disappointing, judging by the number of policy failures, the small tonnage of CO2 emissions avoided or the global trend of rising emissions. But failure analysis can be a powerful teacher.[1] The Wright brothers crashed a few airplanes and had to re-think their design before they built one that could stay aloft even for a short distance. Thus, meticulous analysis of carbon pricing policy experiments would be reason enough to recommend “Can We Price Carbon?” by Barry Rabe, professor of political science at the University of Michigan’s Gerald R. Ford School of Public Policy. But Rabe’s new book offers much more. It’s a thorough, readable, balanced and remarkably well-documented comparative overview of attempts at carbon pricing policy, primarily in North America, with abbreviated examinations of carbon pricing attempts elsewhere, all viewed through the lens of political science.

“A thorough, readable, balanced and remarkably well-documented comparative overview of attempts at carbon pricing policy.”

Rabe, now steeped in climate policy, traces his interest in tax policy as a behavior-modifier to the 1970’s when he ghost-wrote for his father, a Chicago cigar salesman, under pressure to compose jeremiads against tobacco regulation and taxation. Rabe opens his book by sketching the history of excise taxes on tobacco, which in four decades have more than quadrupled the price of cigarettes while funding programs to further discourage smoking, cutting in half the number of cigarettes smoked in the U.S. and reducing the number of new smokers even more dramatically.

After acknowledging the relentless chorus of entreaties from economists imploring climate policy to follow the tobacco example by “putting a price on carbon,” Rabe shows why carbon pricing poses a “super wicked problem” for political leaders. They understandably are reluctant to impose immediate and highly visible costs on their constituents in order to avoid inchoate future harm. And, of course, politicians also face a vocal minority who doubt that global warming is or will become a serious problem. Instead of carbon pricing, elected officials tend to prefer policies like procurement mandates, such as “Renewable Portfolio Standards” (RPS) adopted by more than half of states, requiring utilities to buy a specified fraction of their electricity from “renewable” sources. While RPS mandates offer a lighter political lift and have successfully expanded renewable electricity generation, economists point out that RPS’s represent a hidden, regressive cost, and do not push energy consumers to conserve and improve efficiency. Finally, because RPS’s typically are limited to a set of existing technologies, they do not to tend to spur research and innovation on new options in the way that robust carbon pricing would.

Having set the stage, Rabe launches into “Why carbon pricing has often failed.” For me, as a climate policy advocate, this chapter feels like a spooky graveyard tour, with stops at President Clinton’s “BTU tax,” the 1400-page Waxman-Markey cap-and-trade bill that passed the House but expired in the Senate, Canadian Liberal Party leader Stephane Dion’s ill-fated (perhaps politically suicidal) “Green Shift,” Australia’s carbon tax (enacted, then promptly repealed after a anti-tax wave election), as well as state and provincial efforts including Manitoba and Alberta, the Midwest Greenhouse Gas Reduction Accord as well as the 2016 Washington state initiative, I-732.

The graveyard tour foreshadows several of the book’s recurrent themes. First, the “hubris” of early carbon pricing advocates (including myself) who embraced the compelling economic logic of carbon pricing, hoping that enactment would follow and be “sufficient to launch and sustain it… much as… earlier policies such as Nordic carbon taxes and [U.S.] sulfur dioxide cap-and-trade.”[2] Second, citing Alberta’s carbon tax as an example, Rabe warns that carbon pricing can be “used for symbolic purposes, enabling a government to look good politically through use of a heralded policy tool while not really accomplishing anything.”[3] And finally, Rabe suggests ever-so-gently, that political constraints may not allow carbon prices to rise to levels that would justify eliminating complementary policies such as regulations and mandates.

Barry Rabe, professor of political science at the University of Michigan’s Gerald R. Ford School of Public Policy.

After his graveyard tour, Rabe turns the lights back on with “When Carbon Taxes Work,” focusing primarily on British Columbia’s “textbook” revenue-neutral carbon tax. By 2007, warmer winters in the province had eliminated the extreme cold needed to control the mountain pine beetle, now wrecking highly visible and widespread damage on British Columbia’s prized forests. Responding to public alarm, Gordon Campbell from the centrist Liberal Party campaigned on a carbon tax, inserting it as a “wedge” to win election in a three-way race.[4] Campbell quickly enacted and rapidly implemented[5] the tax, initially set at $10 (Canadian)/tonne CO2 and scheduled to rise to $30 in $5 annual increments. In 2009, Campbell handily won re-election, in what amounted to a referendum on the carbon tax. In addition to its remarkable popularity, several credible analyses concluded that BC’s carbon tax was even more effective than expected at reducing emissions, while BC’s economy grew faster than the rest of Canada.[6]

British Columbia’s Premier, Gordon Campbell enacted the province’s revenue-neutral carbon tax in 2008.

The popularity and durability of BC’s carbon tax is widely attributed to Campbell’s decision to guarantee return of all carbon tax revenue via direct distributions, tax cuts and credits to individuals and businesses. But a skeleton lurks here too. BC’s carbon tax is not revenue-neutral, it’s revenue-negative, bleeding BC’s treasury from the start. It’s becoming a fiscal hemorrhage as subsequent governments have stopped raising the tax rate and added numerous tax “expenditures,” costly exemptions or rebates for special interests including fossil fuel related businesses. Rabe observes, “[c]hronic revenue negativity [of BC’s carbon tax program] may work to further deter future rate increases, given the likelihood that additional revenue would be used to reduce the fiscal imbalance rather than provide new benefits.”[7]

As BC’s carbon tax was ramping up, its shale gas (“fracking”) industry began to boom outside the purview (and carbon-reducing influence) of the tax. Like most carbon taxes, BC’s carbon tax falls on fossil fuel consumers within the jurisdiction; it does not apply fossil fuel produced for export. This underscores a key point Rabe makes later in the book about the advantages of severance taxes imposed on fossil fuels at the point of extraction. Measured in total revenue, state severance taxes imposed by fossil fuel producing states are by far the largest “price on carbon” in North America.[8] Seven, largely “red” states, including Alaska, North Dakota, Wyoming, Oklahoma and Texas have established durable and politically popular sovereign wealth trust funds. Texas and Wyoming rely heavily on trust fund revenue to support education.[9] Unlike carbon taxes or cap-and-trade systems that impose costs on in-state consumers, severance taxes offer a unique political advantage: they fall primarily on out-of-state fuel consumers. Long before anyone proposed carbon taxes, severance taxes were established as important and reliable revenue sources in energy-producing states. In the 1980’s, when severance taxes faced threats of federal preemption, Wyoming Senator Malcolm Wallop thundered, “No one can calculate the impact of oil loss, of erosion, of loss of habitat for wildlife. Who makes the judgment that it exceeds legitimate social costs? Have you been to Wyoming and seen those social costs?”[10] As Wallop’s quote vividly illustrates, a severance tax can build its own political constituency even in conservative energy-producing jurisdictions. A severance tax on BC’s shale gas production could surely offer enormous benefits, perhaps dwarfing the revenue and climate benefits of its now-stagnant carbon tax.

Having offered British Columbia as a hopeful example of a carbon tax that worked (at least initially), Rabe plunges into examination of two U.S. cap-and-trade policies that have endured and enjoyed a modicum of success. In the Regional Greenhouse Gas Initiative (RGGI) an interstate emissions trading system covering the electricity sector in ten northeastern states,[11] over-allocation of “allowances” (permits to emit CO2) has resulted in tiny prices (approximately one fifth of the price set by British Columbia’s explicit carbon tax), leading some observers to characterize RGGI as a “toy” or a “joke” of a cap-and-trade system. In response to such concerns, RGGI added a $2/T CO2 price floor which could be gradually raised to provide a more robust price signal while also augmenting its revenue stream over the long term.

Despite RGGI’s anemic price signal, Rabe suggests that it “revolutionized” cap-and-trade into a revenue-producing system by auctioning all permits, rather than distributing most of them for free to emitters as previous cap-and-trade systems including the European Union’s Emissions Trading system (“EU ETS”) did and the 2009 Waxman-Markey bill would have done. Full auctioning of permits provides a steady stream of revenue for states to dedicate to energy efficiency, renewable energy and demonstration projects that have proven politically popular, contributing to the durability of RGGI, which at 16 years old, has outlasted every other cap-and-trade policy in North America. RGGI’s efficacy at reducing emissions remains less clear; but one particularly enthusiastic study concluded that the region’s emissions would have been 24% higher without the program.[12]

Gov. Schwarzenegger signs AB-32 into law in 2006.

Next up is California’s cap-trade-offset program, AB-32 which Professor Rabe aptly describes as “a work in progress.” California chose cap-and-trade in part to work around the state’s requirement of a two thirds legislative majority to enact tax measures. The resulting legislation and regulatory framework starkly represent the antithesis of a simple, explicit carbon tax. By all accounts, AB-32 could not have launched and or been sustained without the diligent efforts of Mary Nichols, chair of California’s Air Resources Board (CARB), an agency whose resources and depth of expertise remain essential to administer the multi-faceted program.[13] As in the EU ETS, “offsets,” which credit emissions reductions or carbon sequestration beyond the capped entities, offer an alternative compliance mechanism for emitters who would otherwise be required to buy allowances. Cheap and often questionable offsets have raised serious questions about the environmental integrity of California’s program. In response, CARB ratcheted up its oversight of offsets and cut the fraction of offsets available in its carbon market.

California’s attempted linkages with other jurisdictions have also proved problematic. The latest is a link with Quebec which seems to be seeking new markets for its abundant hydro-electric power. Because much of California’s electricity is supplied from out of state, apparent “resource shuffling” to provide “renewable” energy to California while increasing fossil fuel generation for other states has raised concerns that net emissions reductions are chimerical. And finally, recognizing that price volatility and extremely low carbon prices undermine the fundamental purpose to “price carbon,” CARB added a “price floor” of $10/T rising 5% above inflation annually. These administrative “fixes” and “patches” illustrate Rabe’s point that cap-and-trade requires ongoing expert oversight and management to be workable and effective.

As with other carbon pricing systems, revenue use dominates political debate about California cap-and-trade system. The lion’s share of auction revenue funds high speed inter-city rail, affordable housing and intra-city transit. California’s ETS faces ongoing challenges from environmental justice advocates who suggest that emissions trading concentrates emissions of CO2 as well as conventional health-damaging pollutants in disadvantaged communities. The Environmental Justice Alliance has called for replacement of California’s cap-and-trade system with a transparent carbon tax. Severance taxes which might provide simpler, more transparent mechanisms to price carbon, have thus far failed to gain enough political traction for enactment.

Even with all its limitations, AB-32 wins accolades, having survived political upheavals, and like RGGI, has provided at least a modest “price on carbon” that could be augmented by revisions to the program, including a more aggressively-rising price floor.

Rabe concludes with a chapter entitled, “A Second Act for Carbon Pricing” describing a range of new and ongoing efforts at the state and provincial levels to enact carbon pricing. Especially noteworthy are severance taxes in North Dakota and Colorado modeled on Norway’s politically-popular severance taxes that fund pensions. Rabe also suggests taxing the carbon content of fugitive methane emissions from shale gas drilling which to date have drastically reduced the potential climate benefits of shale gas as a bridge fuel.[14] Finally, Rabe observes that the political obstacles to carbon pricing in the U.S. are not unique to our political system or culture. Carbon pricing remains challenging everywhere it is being attempted.

After taking in Professor Rabe’s whirlwind tour of carbon pricing history, I was struck by the absence, even after a decade of relentless advocacy by Citizens’ Climate Lobby and more recently by the Climate Leadership Council, of legislation to enact “carbon fee and dividend” anywhere in the world. Perhaps returning revenue in lump sum “dividends” does little to help dissolve the “super-wicked” political dilemma that Rabe neatly articulated in chapter 2. The enactment and durability of RGGI, AB-32 and BC’s carbon tax were all aided by public support for proposals to spend or distribute revenue. Perhaps once a carbon price is established and is funding visible and popular programs, returning the additional revenue generated by a rising price might make political and economic sense.[15] But given its almost total lack of political support to date, one has to question whether “fee and dividend” can serve as a starting point for politically-viable carbon pricing.

P.S. (5/24/18). Alaska’s oil severance tax, which endows the state’s Permanent Fund, enacted by Republican Governor Jay Hammond in 1976, can be viewed as an example of an easily-implemented, popular and durable upstream ad valorem tax that could easily be converted to a more stable carbon tax. The Alaska tax, assessed on the dollar value of the oil extracted rather than its carbon content, is equivalent to about $53/T CO2.* The Fund currently distributes a $1600/month “dividend” to every eligible Alaskan.

* $72/barrel (current oil price) x 35% (Alaska tax rate) x 1 barrel/433 Kg CO2 x 907 Kg/Ton = $53/T CO2. More than double BC’s “textbook” C$30/tonne ($22/T) CO2 tax!

NOTES:

[1] See, Henry Petroski, “To Engineer is Human, The Role of Failure in Successful Design” (1985) extolling the virtues of rigorous failure analysis.

[2] Rabe, “Can We Price Carbon?” at p. 200. As Rabe elucidates in detail, proponents of cap-and-trade as climate policy enshrouded the SO2 and CFC (“Montreal Protocol”) examples into exaggerated mythology that tended to overlook the more intractable problems of reducing CO2 emissions from a vast range of sources for which few ready replacements existed.

[3] See Rabe, “Failing the Performance Test,” pp. 74- 82. The Alberta carbon pricing system “hasn’t reduced a single ton of emissions yet,” according to David McLaughlin, one of Canada’s leading experts on carbon pricing, and former director of National Round Table on Energy and the Economy, in a keynote address to Canada’s Climate Choices Conference in Waterloo ON, February 18-20, 2016.

[4] Of course, the U.S. has no “centrist” party. Thus, the BC example offers little guidance about political strategy here.

[5] Rabe points out that BC’s carbon tax was fully operational in just five months. In vivid contrast, California’s cap-and-trade system with offsets took years to launch even with the heavy (and ongoing) staffing of its Air Resources Board. p. 95 and p. 168-9.

[9] I am grateful for the legal education I received in Texas, whose public universities are generously endowed by the state’s oil severance tax, paid overwhelmingly by gasoline purchasers in other states.

[11] RGGI participants are Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New York, Rhode Island, and Vermont . New Jersey has recently announced plans to re-join RGGI and Virginia is also considering that step.

[12] Rabe, p 157. Citing Brian C. Murray and Peter Maniloff, “Why Have Greenhouse Gas Emissions in RGGI States Declined” An Econometric Attribution to Economic Energy Market, and Policy Factors, Energy Economics 51 (2015).

[15] See, James K. Boyce, “Carbon Pricing: Effectiveness and Equity” (April 2018). Boyce argues for distribution of carbon revenue in equal lump-sum “dividends” to assure political support for continually raising carbon prices to achieve climate stabilization goals and to counteract regressive distributional effects. https://www.peri.umass.edu/publication/item/1069-carbon-pricing-effectiveness-and-equity

Indigenous groups, environmental justice organizations and climate justice organizations are visibly and successfully confronting global warming directly. To cite just one example, in a stunning show of community organizing and popular will, the diverse, highly-visible “keep it in the ground” movement halted (at least temporarily) the Keystone XL pipeline which would have carried crude oil from Alberta’s “tar sands” across sacred indigenous lands, fragile ecosystems and vital drinking water aquifers to reach refineries in Texas for distribution to U.S. and global markets.[1]Extraction of “tar sands,” one of the dirtiest and most carbon-intensive fossil fuels, would damage or destroy much of Alberta’s Boreal Forest. Beyond its intrinsic value as a home to indigenous people and species, the Boreal Forest is a diverse ecosystem that sequesters millions of tons of carbon annually. [2]

To all appearances, mainstream scientific, environmental and policy organizations have been markedly less successful in organizing and spurring action to confront the climate threat. Beginning in 1979, the National Academy of Sciences issued lengthy, peer-reviewed surveys of global warming science. Early NAS reports estimated that continued fossil fuel burning would double atmospheric CO2 concentrations within a century, resulting in 2 deg C of warming. Based on painstaking studies of bubbles in ice cores that reveal CO2 concentrations in Earth’s paleoclimate history, scientists cautioned that 2 deg C of warming poses serious risk of catastrophically destabilizing Earth’s climate.[3] And they warned that even a stable 2 deg C warmer climate would be far beyond the range in which our species (and most ecoystsems on Earth) have evolved and adapted.[4]

Facing the stark realization that continued rapid exploitation of humanity’s chief energy source poses existential risks, some NAS study authors suggested aggressive pricing policy to attack the causes of climate change. In a 1983 NAS report, Yale economist Bill Nordhaus wrote,

“A significant reduction in the concentration of CO2 will require very stringent policies, such as hefty taxes on fossil fuels…”[5]

Alas, Nordhaus and other NAS collaborators deemed aggressive carbon pricing too radical and premature. Instead, their main policy recommendation was “further study.” That’s what has happened. Year after year, decade after decade, scientific studies continue to describe various aspects of the climate problem in ever more meticulous detail, but they largely temporize or abjure discussion of policy solutions. The scientific community’s hedged and often stilted warnings provided an opening for the well-funded climate science “doubt” industry to exploit. The “doubt industry” intones that stringent climate policies would be terribly costly, perhaps even destroying our economy, which the doubt industry asserts is inextricably and permanently tied to fossil fuel consumption. And they claim that nobody can prove that any climate policy is even needed.[6] Economists have pointed out that revenue from carbon pricing can be recycled to eliminate regressive distributional effects and mitigate economic distortions.[7] Despite such assurances, most U.S. politicians, even those concerned about climate have been only too happy to put off those hard choices.

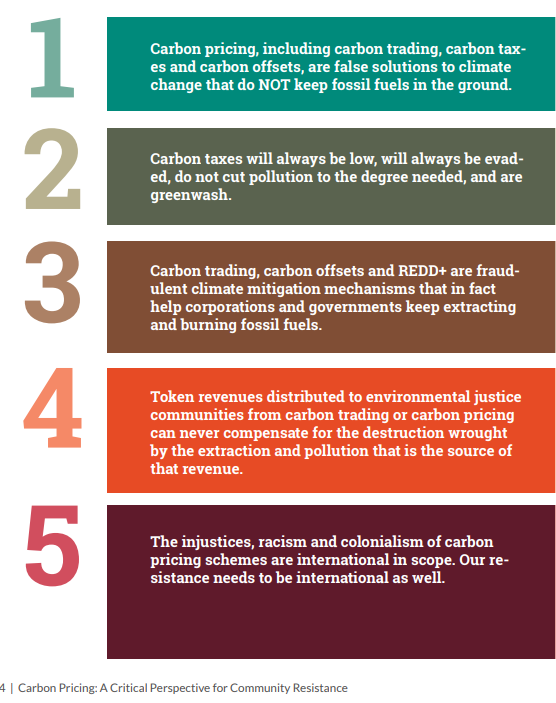

Last fall, a year after the climate movement found itself effectively exiled from the Administration and Congress, a collection of environmental justice, climate justice and indigenous groups issued a “community resistance guide” authored by Tamra Gilbertson, claiming that all carbon pricing is a “false solution.”[8] The “resistance guide” argues, citing substantial empirical evidence and academic research, that carbon pricing, even where enacted and implemented, has not produced the needed shift from fossil fuels to renewable energy and efficiency. (No argument there. We’re just nowhere near where we need to be to avoid climate catastrophe; time’s running out fast.[9])

But a close look reveals that much of the resistance guide’s well-founded critique is based on the flaws and complexities of indirect carbon pricing through cap & trade with offsets. (Hereinafter abbreviated as “CTO.”) I’ve spent a decade researching, writing and advocating simpler, more direct carbon pricing policies that offer fewer hiding places for gimmicks and exclusions and instead provide clear, briskly-rising price signals to investors, innovators and consumers. Instead of auctioning all pollution permits, [10] CTO policies tend to distribute many of them free to polluters in order to grease the skids for enactment.[11] That not only rewards past pollution, it cuts down on the revenue available to compensate disadvantaged communities. And as the guide articulates, the carbon offsets in CTO policies raise serious questions about indigenous rights and equally serious problems of monitoring, reporting and verification which have plagued the European Union’s Emissions Trading System.

Carbon Taxes Are Different Than Gimmicky Cap & Trade with Offsets.

In contrast, transparency, simplicity and an explicit revenue stream are key reasons why carbon taxes remain the most radical climate policy, even though they are grounded in mountains of peer-reviewed economic theory and analysis.[12] Thus, I was distressed that the resistance guide lumps explicit carbon taxes in with complex, gimmicky CTO policies that, as the guide points out, have not induced the robust carbon prices needed for aggressive emissions reductions.

The guide claims carbon taxes can “never” rise to levels high enough to reduce CO2 emissions to the degree needed. It’s true that carbon taxes, as enacted, and even most of those proposed, start too small and rise too slowly to hit consensus climate targets. And it’s true that economic models rarely seem to account for amplifying climate feedback; they discount or entirely exclude catastrophic scenarios so their damage estimates come out low.[13] Twelve years ago, in a widely-cited Scientific American article, Princeton researchers Robert Sokalow and Steven Pacala described a path toward decarbonization broken down into 15 “carbon wedges” whose development and implementation would require a carbon price rising to $100 – $200 per ton within a decade.[14] Eight years ago, a few carbon tax bills were introduced by House Democrats and one brave Republican (Bob Inglis) that aimed that high. Now, I know of no legislative proposals that even come close.

So on the face of it, it’s true that carbon taxes are too small and grow too slowly to have much chance of hitting the kind of climate targets that climate scientists conclude would avoid catastrophic scenarios.

We Need The Engagement of Environmental Justice, Climate Justice and Indigenous Environmental Groups to Enact Effective and Fair Carbon Taxation.

The resistance guide further asserts that carbon pricing, even with substantial revenue directed toward assisting frontline communities, can “never” compensate for the historical environmental harms and future climate damage that disadvantaged communities endure. So the guide jumps to the conclusion that environmental justice, climate justice and indigenous environmental groups should unite to resist carbon pricing on a global scale. That advice overlooks the fact that frontline communities stand to benefit first and perhaps most from policies that mitigate or avoid climate damage. And sticking to the “false solutions” line would leave EJ, CJ and IE groups protesting outside while policy advocates and policymakers develop carbon pricing proposals, work which must be undertaken now if we are to be ready when the political tide turns. And the “false solution” rubric further ignores the robust body of economic analysis showing that regulatory programs, mandates and prohibitions create perverse incentives for other nations to free ride. Even quantity-based carbon pricing systems such as CTO lead to gaming. Only explicit carbon taxes with border tax adjustments offer potential to “go global” by aligning the incentives of nations to trade fairly and push for higher carbon taxes.

The choice between “Keep it in the Ground” and carbon pricing is a false dichotomy. Recent economic analysis suggests that supply side (“Keep it in the Ground”) and demand side (Carbon Pricing) can work well together.[15] The climate movement needs EJ, CJ and IE voices and organizations to keep the pressure on and to engage in designing carbon pricing policy — preferably in the form of transparent, upstream excise taxes on fossil fuel sources of carbon emissions — to assure aggressive prices and fair revenue distribution. Yes, CTO has proven problematic, as many of us warned. But if EJ, CJ and IE voices engage, transparent taxes on climate pollution offer a path to effective climate policy that embraces and enhances climate justice.

Carbon tax advantages emerge from modeling of four climate policy options.