Careful, deliberate analysis of climate policy options and design choices might seem quixotic at a time when climate science is under siege from fossil fuel industry-funded front groups and the Trump Administration is aggressively rolling back climate policy and attempting to subsidize and revive the coal industry. Looking beyond current political obstacles, Lawrence Goulder (Director of the Stanford Energy and Environmental Policy Center) and Marc Hafstead (Director of the Carbon Pricing Initiative at Resources for the Future) offer a detailed quantitative comparison of four leading climate policy options, charting the deep, sometimes murky water of climate policy for the concerned public, climate policy advocates and policymakers.

Careful, deliberate analysis of climate policy options and design choices might seem quixotic at a time when climate science is under siege from fossil fuel industry-funded front groups and the Trump Administration is aggressively rolling back climate policy and attempting to subsidize and revive the coal industry. Looking beyond current political obstacles, Lawrence Goulder (Director of the Stanford Energy and Environmental Policy Center) and Marc Hafstead (Director of the Carbon Pricing Initiative at Resources for the Future) offer a detailed quantitative comparison of four leading climate policy options, charting the deep, sometimes murky water of climate policy for the concerned public, climate policy advocates and policymakers.

Goulder and Hafstead analyze four diverse policy options:

- An explicit carbon tax on coal, oil and natural gas, reflecting the relative CO2 contributions generated by combustion of those fuels.

- Cap & trade. A quantity-based limit on total CO2 emissions. Tradeable permits are auctioned off, indirectly inducing a carbon price.

- A Clean Electricity Standard (CES) specifying the fraction of electricity generated from non-carbon sources.

- A higher gasoline tax.

For the two carbon pricing options, Goulder and Hafstaed emphasize the importance of “recycling” revenue in ways that cut the overall cost of climate policy. Their modeling confirms and quantifies findings of numerous previous studies: Using revenue from carbon pricing to cut other taxes, especially taxes that create large distortions by inducing inefficient allocation and movement of capital and labor or reduced output, can substantially reduce the net economic costs of climate policy.

In a seminal paper published in 1994, Prof. Goulder dubbed the potential for low or no-cost climate policy a “double dividend,” referring to the double benefits of more efficient taxation plus the benefits of reducing unpriced climate, environmental, and public health damage.[1] Goulder and Hafstead’s new analysis concludes that the strong “double dividend,” where net policy costs are zero or negative, is as rare as the economists’ proverbial “free lunch.” It would occur only if the distortions from the tax whose revenue is being replaced by carbon revenue are so large that reducing them overcomes the costs created by a carbon tax: a reduced tax base and interactions with other taxes. But the weak double dividend, where policy costs are reduced (but not overcome) by the efficiency benefits of revenue recycling is far more easily obtained.

Goulder and Hafstead’s E3 (energy-economy-environment, general equilibrium) model reveals the weak double dividend whenever carbon revenue is used to replace other distortionary taxes. By far the largest efficiency benefits arise from using carbon tax revenue to cut corporate income tax rates. Using carbon revenue to cut individual income tax rates produces modest efficiency benefits while cuts in employee payroll tax rates offer slightly smaller efficiency benefits. Returning revenue in lump sum fashion produces little or no efficiency benefit.

Alas, while Goulder and Hafstead were assiduously analyzing the benefits of recycling revenue from carbon pricing and (presumably) rushing to publish their results, Congress and the Trump Administration cut the marginal corporate income tax rate from 32% to 21%,[2] knocking much of the distortionary edge off U.S. corporate taxation. Nevertheless, given the robust economic literature suggesting a large excess burden[3] from taxes on capital compared to other taxes such as income and payroll taxes, their ranking of the relative benefits of various tax shifting proposals should stand, even if some of their quantitative results have been overtaken by events.

Goulder and Hafstead articulate and quantitatively illustrate the stark tradeoff between economic efficiency and distributional equity in the design of climate policies. They stress the need to account for both the regressive use-side impacts of carbon taxes, as well as their progressive source-side impacts. Their model includes both, providing a ranking of revenue options for distributional progressiveness which reverses the order of their ranking for economic efficiency. Lump sum rebates are most distributionally-progressive, followed closely by reduced employee payroll taxes and reduced individual income taxes. Finally, they find that reduced corporate income taxes are the least progressive option, though not necessarily regressive as commonly assumed. Goulder and Hafstead also analyze hybrid options: using a fraction of revenue to compensate households in the bottom two income quintiles while using the balance to reduce corporate income tax rates, similar to the carbon tax measure proposed by Rep. John Delaney (D-Md).[4] As expected, these hybrids produce intermediate effects, trading off some efficiency for distributional equity.

Goulder and Hafstead conclude that at low CO2 abatement levels, a Clean Electricity Standard (CES), which effectively sets a “floor” on the fraction of non-fossil fuel generated electricity,[5] can be cost-effective even when compared to carbon pricing mechanisms. But they point out that carbon pricing surpasses the efficiency of a CES as CO2 abatement goals become more stringent over time. One key reason is that unlike a carbon price, a CES does not provide a price signal to electricity consumers to encourage conservation and efficiency. In effect, a CES amounts to a tax on fossil fuel energy, plus a subsidy to non-carbon energy, leaving consumer electricity prices essentially unchanged. And, of course, a CES is limited to the electricity sector, leaving out the industrial and transportation sectors, creating distortions across the economy.

Finally, Goulder and Hafstead analyze the climate benefits of raising the gasoline tax. They conclude that while higher gasoline taxes do produce benefits that exceed their costs, especially when non-climate co-benefits are considered, higher gasoline taxes do not offer anywhere near the potential that economy-wide carbon pricing offers to reduce emissions. In fact, they conclude that while each of the other three policies could be designed to bring the U.S. close to meeting its commitments under the Paris Climate Accord, no conceivable increase in gasoline taxes could achieve that alone. Nevertheless, I might suggest modeling a gasoline (and diesel) surcharge added to an economy-wide carbon tax to compensate for the relatively low price elasticity in the transportation sector that makes it less responsive to carbon pricing than the rest of the economy.

“Confronting the Climate Challenge” is written in somewhat technical language, but even to a lay reader, the book clearly illustrates economic concepts graphically and with salient examples. Goulder and Hafstead’s description of their E3 model and tabulations of results offer readers a look at how their general equilibrium model works, and gives a sense of the granularity of their analysis. The model divides the economy into roughly 40 industrial sectors; tabular results show the effects of various policy and revenue options on those industries. Graphical illustrations of distributional and regional costs and benefits flesh out the picture and remind us that design details can indeed matter just as much as policy choice.

The four relatively diverse policies chosen by the authors seem to be the most politically viable both on the state and federal level. With progress on climate policy stalled at the federal level, states are showing increased interest in carbon taxes, cap-and-trade systems, clean energy standards (including the Northeast States’ Regional Greenhouse Gas Initiative). Even the long-taboo subject of raising gasoline taxes has come up in the context of infrastructure funding.[6]

Goulder and Hafstead take pains to point out that well-designed cap-and-trade systems can price carbon pollution as efficiently as carbon taxes, though they do not mention carbon offsets, an almost ubiquitous design element of cap-and-trade systems that has thwarted their effectiveness as price-setting mechanisms. Similarly, the authors do not mention the effect of price volatility which tends to muddy price signals and cloud long term price expectations in cap-and-trade systems.

In their conclusion, Goulder and Hafstead mention that their modeling treats the rate of technological innovation as an exogenous variable. Thus, to the extent that carbon pricing induces or accelerates low- or non-carbon energy innovation, their estimates may understate the effectiveness of carbon pricing.

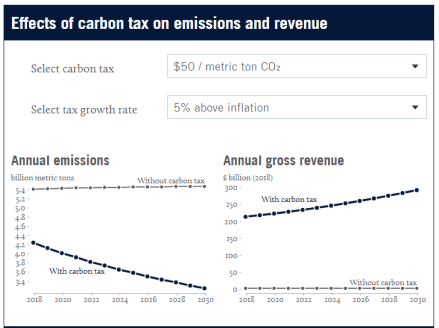

Goulder and Hafstead also mention the possibility of preempting some existing (presumably redundant) climate policies if carbon pricing were enacted, noting that this would produce additional efficiency benefits.[7] If Goulder and Hafstead’s carbon tax rates ($10, 20 and 30/tonne CO2 with a 4% annual increment) were more aggressive, the suggestion to preempt redundant policies might be more persuasive. They do not even attempt to model more aggressive carbon pricing (which if adopted globally) could offer a path to emissions reductions consistent with the IPCC’s 2 deg C target discussed in the book’s introduction.[8] Perhaps even more frustrating, Hafstead’s elegant and easy-to-use online carbon tax calculator[9] does not even allow carbon taxes that start higher than $50/ tonne or rise more briskly than 5% annually.

Surely, if economy-wide carbon taxes with revenue recycling are indeed the most cost-effective and thus the most potent policy option, we should be encouraged to consider more aggressive options to reduce the risks of catastrophic scenarios including tipping points and amplifying feedback.[10]

NOTES:

[1] “Environmental Taxation and the Double Dividend: A Reader’s Guide,” Lawrence H. Goulder, NBER Working Paper No. 4896, October 1994. http://www.nber.org/papers/w4896

[2] “Final Version Of GOP Tax Bill Cuts Corporate Tax Rate To 21 Percent,” NPR, December 15, 2017. https://www.npr.org/2017/12/15/571257526/final-version-of-gop-tax-bill-cuts-corporate-tax-rate-to-21-percent

[3] The excess burden (or degree of distortion) is a measure of unintended behavior (and resultant economic) changes induced by a tax beyond its revenue-generating effect. Corporate income taxes are considered more distortionary than other taxes because (at least until recently) marginal tax rates on returns to capital have been relatively high, and business actors tend to have better information and ability to shift investments and business activities to avoid or reduce taxes. See e.g., “Excess Burden of Federal Taxes Imposes High Economic Cost,” Joint Economic Committee Report #110-8, June 2007. https://www.jec.senate.gov/public/_cache/files/d99ac41c-bd86-4826-8623-ae68af9c3577/excess-burden-of-federal-taxes-imposes-high-economic-cost—june-2007.pdf

[4] “Tax Pollution, Not Profits Act,” https://delaney.house.gov/news/press-releases/delaney-files-carbon-tax-bill-revenues-used-to-lower-corporate-tax-rate-provide

[5] Some CES designs credit utilities that switch from coal to natural gas generation, recognizing the lower CO2 emissions from gas. See e.g., RFF analysis of Senator Bingaman’s 2012 CES proposal. http://www.rff.org/files/sharepoint/WorkImages/Download/RFF-DP-12-20.pdf

[6] One wonders if there would be any net environmental or climate benefit from increasing the gasoline tax in order to fund more fossil fuel and automobile infrastructure, a question not raised in the book.

[7] Goulder & Hafstead, p. 236.

[8] After noting that the IPCC goal of stabilizing warming below 2 deg C would require emissions reductions in the range of 40 – 70 % by mid-century and reduction of emissions to near zero by 2100, Goulder & Hafstead indicate that they only attempted to model carbon taxes that would reduce emissions 45% below their 2013 baseline by 2050. (Chapter 8, footnote 1, p. 326.)

[9] See “Introducing the E3 Carbon Tax Calculator: Estimating Future CO2 Emissions and Revenues,” Marc Hafstead, Sept. 25, 2017. http://www.rff.org/blog/2017/introducing-e3-carbon-tax-calculator-estimating-future-co2-emissions-and-revenues

[10] See “National Climate Assessment,” U.S. Global Change Research Program, Washington, DC, November 2017. In particular, chapter 15, “Potential Surprises: Compound Extremes and Tipping Elements.” https://science2017.globalchange.gov/downloads/CSSR2017_FullReport.pdf

Nice and helpful review, James! Do the authors parse household net-welfare effects (averages or by state and income level) in different scenarios?

LikeLike

Thanks Alex. Yes, chapter 7 offers state-by-state comparisons of effects on business profits as well as detailed analysis of distributional impacts on households (grouped by income quintile) for various future years and integrated over selected time intervals. As you’d expect, they find that choice of revenue return option changes regional distribution and income distribution noticeably, though the magnitudes are not large. Differences are in the single digit percentages, most in the low-single digits.

Most striking to me was the adverse effect on coal states, which underscores the suggestion our friend Adele Morris has made that a share of carbon revenue be directed toward transition assistance in coal regions.

LikeLike

It was very gratifying for me to see this review by James of my book with Marc Hafstead. From the review it was clear that James had examined the book exceptionally carefully and that he had a deep understanding of the issues. Beyond appreciating the compliments, I found his original comments and suggestions very insightful. In particular, I believe James is on target when he claims that, subsequent to the recent tax reform, the benefits from corporate income tax recycling are likely to be smaller than what we found in our book. Marc and I are likely to re-analyze the recycling potential of corporate tax recycling in future work. I also like James’s suggestion of having a closer look at carbon tax policies that are somewhat more aggressive than the policy that forms the central case in our book. Although the political challenges might well increase with the boldness of a proposed carbon tax policy, most economists conjecture that a carbon tax time-profile higher than the central case profile in our book would yield the highest net benefits. To me, this justifies a closer look at the higher time-profile. In fact, Marc and I have already started to take the closer look.

LikeLike